Tracing Support Networks That Refine Income-Tied Billing Cycles in Barrier-Free Lending Without Upfront Scrutiny

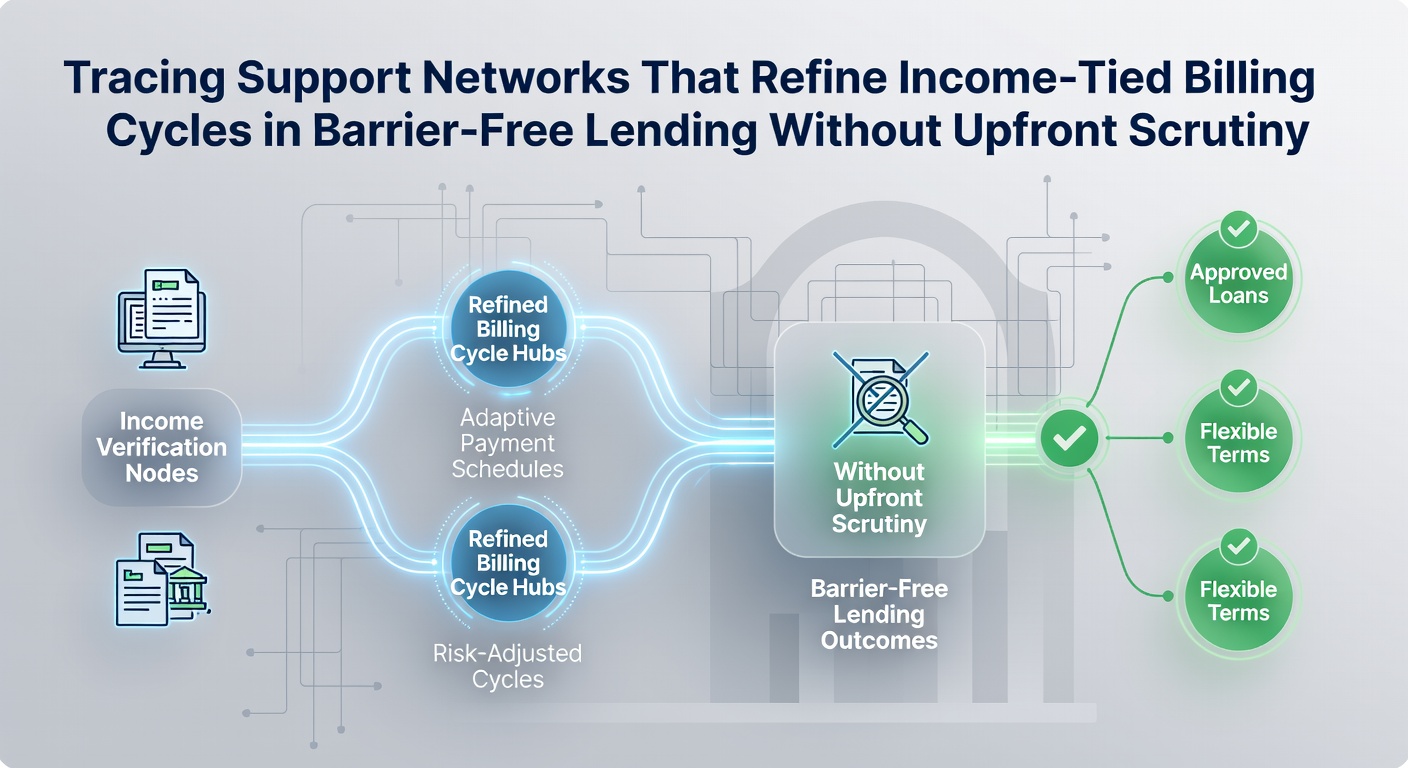

Support networks in barrier-free lending operate through interconnected systems that link borrower income data directly to repayment schedules, and these arrangements bypass traditional credit evaluations by relying on real-time verification methods instead. Data from financial institutions shows that such networks process adjustments monthly, often using automated feeds from payroll services or bank accounts to calibrate amounts owed based on earnings fluctuations.

Researchers at various academic centers have mapped these structures, noting that they typically involve third-party advisors who coordinate between lenders and borrowers to maintain compliance while allowing variable payments. In practice this means a borrower experiencing a temporary income dip might see their billing cycle stretched automatically without needing to submit new applications or undergo repeated reviews.

Core Components of These Networks

Income-tied billing cycles emerge from layered partnerships that include technology providers, compliance monitors, and advisory teams, and each layer contributes specific functions to keep the process seamless. Technology providers supply the algorithms that detect income changes, while advisory teams handle communication to ensure borrowers understand upcoming adjustments before they take effect.

Studies conducted across multiple jurisdictions indicate that these components reduce processing delays compared to conventional lending models, with some networks achieving same-day recalibrations when income reports arrive. Observers note that the absence of upfront scrutiny shifts the verification burden to ongoing monitoring, which relies on secure data-sharing agreements rather than one-time credit pulls.

Operational Mechanisms in Practice

Tracing these networks reveals a sequence where initial loan activation occurs rapidly, followed by continuous income tracking that feeds into billing refinements. Lenders integrate APIs from employment databases or accounting software, allowing monthly cycles to reflect actual earnings without manual intervention each period.

One documented case involves a mid-sized fintech platform that partnered with payroll processors to automate adjustments, resulting in billing amounts that varied by up to 40 percent month to month according to reported figures. Regulatory updates scheduled for May 2026 in several regions aim to standardize data privacy protocols within these systems, requiring clearer consent mechanisms for income data access.

Advisory support within the network often includes scheduled check-ins, and these interactions focus on explaining how income variations translate into payment changes rather than assessing creditworthiness anew. Evidence from industry reports shows that borrowers in these arrangements maintain higher retention rates when support teams provide proactive notifications ahead of cycle shifts.

Geographic Variations and Regulatory Influences

Different regions approach these support networks with distinct oversight frameworks, and the European Banking Authority has issued guidance on transparency requirements for variable repayment structures that do not involve preliminary credit assessments. Meanwhile Canadian regulators emphasize consumer protection through mandatory disclosure of how income data influences billing cycles.

Australian Securities and Investments Commission data reveals that barrier-free lending products with income-linked features grew steadily through 2025, driven by networks that connect borrowers to flexible repayment options without traditional barriers. These variations highlight how local rules shape the depth of support services available within each network.

Integration of Technology and Human Oversight

Modern implementations combine algorithmic monitoring with human advisors who step in when income patterns deviate from expected ranges, and this hybrid model allows networks to refine billing cycles while addressing edge cases that automation alone might miss. Research papers from university finance departments document how such integrations lower error rates in payment calculations over time.

Networks also incorporate feedback loops where borrower inquiries prompt system updates, ensuring that income-tied adjustments remain accurate across diverse employment situations. Those who've examined transaction logs from multiple platforms find that these loops contribute to fewer disputes when cycles shift unexpectedly due to seasonal work or variable hours.

Conclusion

Tracing support networks that refine income-tied billing cycles demonstrates how interconnected systems enable barrier-free lending without upfront scrutiny by prioritizing continuous verification and adaptive adjustments. As regulatory developments in May 2026 take effect, these networks will likely incorporate enhanced privacy standards while maintaining their core function of aligning repayments with real earnings patterns.

Further examination of these structures continues to provide insights into scalable alternatives for borrowers seeking flexible arrangements across different lending environments.